Venture Forward

Recapping 2023 revelations and looking towards a brighter 2024 in the VC ecosystem. Exploring the Red Queen Hypothesis, The Lollapalooza Effect and a world where only the strongest companies survive.

Executive Summary

As we stepped into 2023, the venture capital landscape was already marred by underwhelming deal activity, fundraising efforts, and IPOs. This challenging start of the year was further exacerbated by the collapse of Silicon Valley Bank and shifting geopolitical landscapes.

I became a full-time growth stage investor just two years ago…nothing like joining at the top.

One of my favorite investors, Charlie Munger (R.I.P), Warren Buffett's long-time partner at Berkshire Hathaway, coined the term the Lollapalooza Effect. It refers to a situation where multiple factors, tendencies, or influences converge to produce an extreme outcome. In 2023, it felt like there was convergence of negative expectations where a significant number of investors, LPs, analysts, and industry leaders began to predict a downturn and this collective expectation turned into a self-fulfilling prophecy.

The heightened sense of investor caution created a perfect storm, preventing the venture capital sector from gaining any favorable momentum throughout the year.

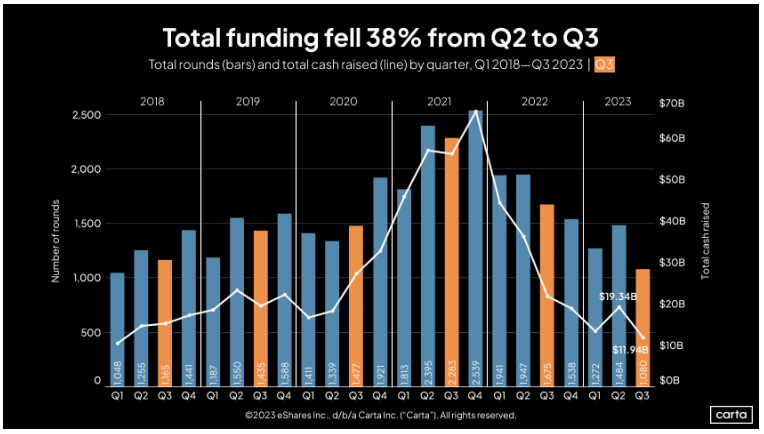

The third quarter of 2023 was particularly stark, marking near-historic lows in both A) the value of venture deals and the B) number of transactions – the lowest in six years and three years, respectively.

According to Carta, there was a major downturn in the startup ecosystem, with a 38% drop in capital raised and a 27% decline in venture fundraising rounds from the second to the third quarter. Notably, nearly one in five investments recorded was a down round. This decline in VC funding marks a consistent downtrend observed in six of the past seven quarters.

From data provided by Pitchbook, a closer quantitative analysis of deal trends over the last 18 months also reveals significant shifts. And although the equity capital market is operational with some significant IPOs, a cautious approach prevailed among many investors and issuers, opting to wait rather than move forward in the process. This reduced market activity has led to an accumulation of assets, with private dry powder (of $290B+ in the VC ecosystem and $1T including VC & PE) reaching unprecedented levels.

A shift happened in the internal valuation landscape too. For the first time in over six years, more than half of the companies undergoing new 409A valuations on Carta saw no change from their previous assessments. Flat valuations, which have been a common occurrence for several quarters, became the majority in Q3, with a stable 409A valuation being almost twice as likely as an increase.

There has been a slowdown in the venture ecosystem.

I also feel part of this slowdown can also be attributed to investors spending more time with their existing portfolio companies, especially those where investments were overvalued in the post-pandemic exuberance. At Expanding Capital, we have been helping companies with operational efficiencies and GTM/sales.

In short, the trajectory of 2023 had been undeniably challenging.

Of course, in a world of ‘alternate facts’, there is positive data, too. I came across a report from Ramp & AngelList that noted there's been an uptick in startup funding, with 8% of startups on AngelList securing funding or achieving exits in the third quarter of 2023. Of course though, the key driver behind this positive momentum appears to be the surge in investments directed towards AI and ML startups.

As we venture forward, I hold a brighter view for 2024. SVB research flagged that, “Historically, 12-18 months into a down cycle VC investment reaches a floor. While US VC investment levels may still fall, they are showing signs of stabilizing”.

What follows is a recap and my perspective on 2023 – where we’ve been– and my forecast for 2024 – where we’re going. In this essay here, I look forward to sharing the key trends that are shaping my outlook for the coming year.

Where We’ve Been

Seed/Early Stage

At Expanding Capital, we typically invest at Series B and above, and in companies with recognized ARR greater than $5M. However, for this research I wanted to understand trends from seed to IPO, and how it all impacts our firm and industry.

For pre-seed and early stages, the latest data from Pitchbook reveals a consistent trend in pre-seed and early stage valuations. As of 2023 year-to-date, the typical deal size and pre-money valuation stand at $500,000 and $5.7 million respectively, mirroring the figures from 2022.

Interestingly, while the median size of seed deals has hovered around $3.0 million for the past five quarters, there was a noticeable uptick in the third quarter of 2023, with the median reaching a new high of $3.3 million. This increase likely reflects a strategy among founders to extend their financial runway and delay the need for further fundraising in the early stages.

Despite the challenges in the broader market, the pre-seed and seed segments have shown resilience. A combination of formula-driven deal structures, like SAFE notes, a focus on more qualitative due diligence, and the abundance of emerging managers and mega seed funds have helped sustain and even boost key deal metrics.

I also believe layoffs, RIFs, employees being underwater on options have caused more people to start a company. As a fun example of this, I saw this tweet from one of my favorite pre-seed investors, Jenny Fielding, “3 people at our Thanksgiving dinner expressed dissatisfaction with their jobs / career trajectory. By the time dessert was served, we had worked out a relevant startup idea for each of the 3 people, complete with biz model, GTM strategy and funding options. Sometimes I feel like a cult leader slowly converting unsuspecting employees into startup founders”

While researching this essay, I learned a new concept called “Relative Velocity of Value Creation” or RVVC, which is the percentage change in valuations between round per years. In the realm of early stage investments, the narrowing difference in valuations between seed and early-stage ventures has led to a significant drop in the rate of value creation, as indicated by the RVVC figure reaching a 10-year low of 35.3%. This change is likely due to investors prioritizing startups with solid financials and clear paths to profitability even…. in earlier stages. A common trope I hear is $1M ARR in the first 12 months; this threshold might lead many startups to opt for bridge rounds over new series rounds if they don’t hit the $1M ARR number. For startups, maintaining or increasing valuation across fundraising rounds is essential. A failure to do so can raise red flags for investors.

To address this, many early-stage companies are extending the time between financing rounds to ensure growth and achieve valuations that will attract new investors. This makes it harder for us, as early growth or late stage investors to see deal flow with more companies waiting to raise venture dollars.

Growth Stage

There’s great data from Pitchbook, Crunchbase, and Carta below; I’ll get to that. However, first let me share some proprietary data. I use a deal-focused CRM called Affinity to manage my deal pipeline. When I compare 12/1/2020-12/1/2021 to the last 12 months, as a firm, we saw a 20.23% decrease in deal volume. In 2020-2021, we took 3.64% of deals to terms. However this last year, zero net-new deals made it to terms; I interpret this to mean while volume was down, so was the quality of companies we saw.

I feel that the most effective founders are those immersed in building their businesses and catering to their users needs, rather than focusing primarily on meeting new investors. The best founders slowed burn, hunkered down, and just built.

The 2023 state of late-stage startup valuations, as reported by Pitchbook, illustrates a unique scenario within the venture capital ecosystem and mirrors our own data. In 2023, the average time between funding rounds for late-stage startups was extended to 1.72 years, the longest interval among all stages. This trend was partly due to the substantial capital these companies accumulated, allowing many to navigate through the current challenging deal-making climate without the immediate need for new capital. The late-stage startups that have re-entered the market in recent times likely secured their last rounds of funding during the high-valuation period of late 2021, and their successful fundraising efforts in the third quarter have led to an increase in the median pre-money valuation to $63.0 million.

In looking at our portfolio of growth stage companies in the last year, only a handful went to market for new capital.

The late-stage market faces intense competition, exacerbated by the substantial number of late-stage companies, from Pitchbook, approximately 15,000 as of the third quarter of 2023. This figure has grown by 5,000 since the beginning of 2020, making an already competitive environment even more challenging. Despite these hurdles, many late-stage startups have grown considerably, developing robust revenue streams that enable them to more effectively manage their cash flow and reduce their reliance on external funding. Unfortunately, many of these companies have had to RIFs, or layoffs, or slow marketing spend, but they have revenue coming in to offset this.

However, the increased median time between rounds, now at also 1.72 years, suggests that these companies secured their previous funding at the height of valuation levels in late 2021 and early 2022. The number of estimated down rounds has risen significantly, reaching a near-decade high of 17.1% in Q3, although a considerable number of companies are still managing to raise funds at higher valuations, positively influencing overall deal metrics.

Pre-IPO

The current scenario at very late stage companies, as detailed by Pitchbook, paints a complex picture of this particular stage in the venture capital landscape. Despite a few high-profile venture capital-backed companies going public in 2023, such as ARM, Instacart, and Klaviyo, their underwhelming performance in the stock market has made many venture-growth startups wary of public listings as a liquidity strategy. Many Pre-IPO companies are now opting to prolong their financial runways by reducing staff and other variable costs, while also exploring alternatives like acquisitions. Consequently, the median duration between funding rounds has stretched to a five-year peak of 1.46 years, as these startups try to delay the need for additional capital.

For those late stage startups that returned to the market, the reality was stark. This stage has seen the most significant drop in valuations across all venture stages, with the 2023 year-to-date pre-money valuation plummeting to $129.6 million, down 65.2% from the high of 2021. It makes sense, public multiples have adjusted sharply.

The decrease in liquidity options have empowered active investors to negotiate for larger equity stakes, pushing the median equity stake for 2023 to a ten-year high of 14.9%. The unstable macroeconomic environment has even led some venture-growth startups to the brink of bankruptcy, as they struggle to raise new capital or find buyers.

One example is one of our portfolio companies whose name I won’t mention. This was a fast growing company, doubling every year but unprofitable. KPIs shifted and they had to go to market, but raised at a 50% discount rate from their last round.

Another example of the dire situation is the Seattle-based trucking startup Convoy, once valued at $3.8 billion, which ceased operations after failing to secure a buyer or additional funding.

For the most part, these late stage startups have some leeway in timing their fundraising efforts, thanks to their significant capitalization in recent years and their larger scale operations that help manage high monthly expenses. Nevertheless, securing funding in this challenging environment is noteworthy. If this tough deal-making environment persists, we may witness more such promising startups falter, and I will talk more about this below.

The third quarter was saved from a further decline in deal value by Anthropic’s $4 billion deal with Amazon, though this does not signify a broader recovery in capital availability. Investors are increasingly focusing on quality, resulting in a slowdown in deal-making across the venture lifecycle. The number of megadeals, each worth over $100 million, had remained low in recent quarters, with only 30 in Q3 compared to 43 in the same period last year. This reflects the challenges late-stage startups face in securing equity financing, leading many to opt for cost-cutting measures like layoffs. The median annual deal size for venture-growth startups currently stands at $11.4 billion, just a third of the $31.0 billion median in 2021 and the lowest since 2016.

In the current environment, where high interest rates prevail, investor sentiment is shifting towards valuing profitability and solid financial metrics over aggressive growth. As investors favor alternative investment options, they are increasingly drawn to startups that demonstrate a clear path to profitability and long-term financial stability. However, the lack of exit opportunities for these mature companies is limiting return potential for investors, causing a slowdown in their investment pace.

Carta’s data reinforces this t rend, indicating that the interval between funding rounds is increasing. For instance, startups that secured a Series C round in Q3 had waited over three years since their Series B, on average. This extended duration between rounds necessitates that startups efficiently utilize their existing capital. This is also a reason why our deal pipeline was down from prior years.

Secondary Market

Two years ago, at Expanding Capital, we started closely analyzing the secondary market, when new primary growth deals hit a standstill. I published my initial research on creating my own Bid/Ask spread model here. As a firm, our initial goal was straightforward: to understand the real valuations of private companies. But soon, we saw an opportunity to invest in these companies at significantly lower prices than their last funding rounds. Take Stripe, for example – we jumped into a secondary deal in the business.

Data from Addepar shows that the secondary market for venture-backed firms has been growing. More firms entered the secondary market at revised prices in Q3, continuing the trend from Q2. Shareholders in successful companies had good chances for liquidity as buyer interest in high-quality companies at reasonable valuations rose. Price variations remained though, with some deals showing a 100% premium over the last round and others dropping to a 75% discount. The average discount was about 44%, up from 60% in Q2. Prices varied widely depending on the company and deal structure.

With public markets just barely open, exit uncertainty kept pushing more sellers into the market, matched by an increase in buyers. This led to more activity in Q3 reported by Addepar. Shareholders, including GPs, were torn between cashing out at current valuations or waiting for future gains. GPs were actively looking for ways to generate profits to pay back investors and sometimes to avoid holding onto their least liquid assets until the end of their fund’s life cycle, in other words, get DPI.

In the LP-led part of the market, buyers and sellers struggled with wide bid/ask spreads. In the GP-led part, buyers wanted higher returns and more security. Despite these issues, the appetite for investment remained strong, with capital flowing into diversified LP portfolios and top assets. A Lazard report confirmed these trends. It showed continued pricing challenges in the LP-led segment and a demand for higher returns in the GP-led segment. Total deals in the first half of 2023 reached about $43 billion, down 28% from the first half of 2022, with GP-led deals making up 40% of this. Single-asset deals were generally more favorable, with 60% pricing at or above par, compared to just 5% in the LP-led deals, highlighting a strong demand for high-value businesses.

Where We’re Going

In the world of growth stage investing, there's been a palpable shift in the air. Over the past year, many venture capitalists, like myself, have observed a decline in both the volume of companies seeking funding and the perceived quality of these companies. Now, the key question I’m asking is:

How will macroeconomic forces impact private, growth-stage investing in the near future?

From the economy, pent-up dry powder, AI, and more, I have a slightly more optimistic view ahead.

Strong Economy?

The U.S. economy is demonstrating remarkable strength, we just had a record-breaking Black Friday and Cyber Monday. We also have had a strong GDP report, strong ongoing job growth, and a rising stock market, and the picture is….. actually one of a strong economy?

The stock market is flourishing. The current upswing in the stock market is shaping up to be the most robust since 1985, as evidenced by specific metrics. This alignment between the S&P 500 and Nasdaq 100, both marking consecutive 11-week gains, mirrors a similar synergy last seen in 1985. Currently, the S&P 500, Nasdaq 100, and Dow Jones Industrial Average are all on a nine-week upward trajectory. The S&P 500 is inching close to its record peak of 4,801, now just 1% shy, though it hasn't surpassed this milestone yet. Looking back to 1950, this scenario has unfolded 11 times where the S&P 500 experienced a 20% dip only to rebound to nearly its previous all-time high.

Inflation is showing signs of cooling and expectations of rate cuts by the Fed (more on this below). The (prevailing) optimism in economic circles hinges on the belief that we've already braved the most rapid phase of monetary tightening. Jan Hatzius, the Chief Economist for Goldman Sachs, suggested that economic growth is usually most affected by a sharp hike in rates, typically with a six-month delay. Given we've crossed that timeline, proponents argue, the likelihood of a significant downturn driving the U.S. into recession seems slim, despite some lingering effects of monetary policies. As a contrarian take, my Partner, Mark Dinner, previously a Senior Investment Associate at Bridgewater mentioned that our historical playbook doesn't offer many parallels to our current scenario — a tightening phase amid an abundance of money in the system, coupled with the Federal Reserve's quantitative tightening. One reason the economic drag hasn't hit hard yet could be attributed to households depleting their excess savings. I believe the overall economic health signals a promising environment for VC activity.

Flat (or Decreasing) Interest Rates

Interest rates, a key macroeconomic lever, profoundly influence private company investments. Post the 2008 crisis, central banks globally, including the U.S. Federal Reserve, embraced low-interest policies to spur growth. This era, often termed the "Zero Interest Rate Phenomenon" or ZIRP, has significantly altered the investment landscape. In such an environment, traditional investments like bonds and savings accounts yield minimal returns, compelling investors, particularly limited partners, to seek higher returns through alternative investments. This shift has notably increased the risk appetite among investors, as they gravitate towards potentially higher-yielding, albeit riskier, startups compared to established firms.

Yet, this low-interest rate environment has a flip side – inflation, escalating at rates unseen in recent decades. This surge in inflation heightens operational costs for companies and diminishes consumer purchasing power, thereby hampering corporate growth and profitability, ultimately detracting from their investment appeal.

In response to this, a shift to higher interest rates has ensued, aiming to manage the inflationary spiral. This increase directly affects startups by elevating their cost of capital, essentially the baseline return they must generate to justify their fundraising efforts. This cost encompasses both the interest paid on debt and the expected returns on equity investments.

Beyond economic policies, external factors like geopolitical unrest – the Ukraine conflict, the war in Israel, China tensions – add layers of complexity. These tensions breed market volatility and can escalate operational costs for businesses, impacting their bottom line.

However, peering into 2024, the Federal Reserve's outlook suggests a potential easing of interest rates, with projections indicating a decrease to around 4.5%. This anticipated shift could reignite investment fervor in technology sectors, possibly enhancing valuations. In this scenario, venture capital may regain its stature as a premier asset class, outpacing traditional investment vehicles like money markets, driven by a renewed or amplified interest from limited partners.

Abundant Dry Powder Will Have To Get Deployed

The venture capital landscape is flush with a record $290 billion in dry powder, as highlighted in SVB's State of the Markets report. According to Preqin data, global private equity dry powder stood at $1.5 trillion at the end of 2020. This abundance of capital on the sidelines reflects a certain hesitancy. Investors are cautious about deploying capital into private companies given the economic uncertainty. However, this unprecedented capital reserve can also ignite new funding rounds. The sheer scale of this unallocated capital mandates a strategic deployment, setting the stage for an active investment period. Funds that have been raised in 2018 or 2019, will have obligations to deploy which I believe will activate the VC landscape.

AI Investments & Efficiencies

In 2024, AI will remain at the forefront. Crunchbase documented that in 2023 AI-focused US startups captured over a quarter of all investments. In 2023, every fourth dollar invested in US startups flowed into AI ventures. To put this in perspective, between 2018 and 2022, AI startups were cornering an average of 12% of funding capital. Fast forward to 2023, and we saw funding for AI-related startups skyrocketing past the $23 billion mark. I believe the AI investing trend will continue in 2024 as companies continue to get traction.

However, beyond just investment dollars, I believe the real game-change lies in AI's capacity to redefine startup efficiency across various business domains - from engineering, human resources, recruiting to accounting, creative domains, marketing, and copywriting.

AI's role in these segments is not just about automation; it's about reinventing operational models to enhance profitability. By streamlining processes and cutting operational costs, AI paves the way for startups to achieve improved margins. This efficiency isn't just a matter of internal mechanics; it fundamentally can alter the financial health of businesses. More profitability leads to more attractive investment multiples, creating a robust, investment-worthy business landscape. This convergence of technological advancement and business efficiency marks a new era where AI is not just a tool, but a transformative force in the startup ecosystem.

Investing Beyond TMT

In the growth-stage venture ecosystem, breakout software companies are easily identifiable. These companies all exhibit strong growth rates (70-100%), high gross margins (80%+), and substantial NRR (130%+). But, going forward, gaining allocations in these deals will become harder to get access to.

As a result, 2024 will continue to push growth-stage investing more akin to true venture investing, requiring investors to make more substantial, venture-style investments to achieve higher returns. I mean more investors will invest beyond TMT; everything else and software.

There is less capital chasing these ideas and in order to get asymmetric returns for our LPs, we must look beyond steady state software. We're spending more time on cloud infrastructure, which includes semiconductors, as well as robotics, climate, food, industrials and defense tech (especially with a focus on American optimism).

I had a conversation with John Fogelson, from Friends and Family VC. He made an interesting point. “What we call deep tech today, in the 1970’s we just called venture capital. We should be filling the void where bank capital will not flow”

Deep tech is a growing sector in the venture capital arena, doubling its share to 20% over the past decade, according to BCG; I suspect it will grow even more this year.

The venture capital space will have to evolve to embrace more 'venture-like' opportunities, signaling a shift away from more traditional, less risky or steady state investments like software. According to Crunchbase's data on $1 billion startup exits in 2023, about a quarter of these high-value exits are in the deep tech space. This points to a growing interest and potential for substantial returns in this area.

Only the Strong Survive

I believe we haven’t seen the bottom yet, and I’ll tell you why this is a positive.

One of my favorite frameworks is called the Red Queen Hypothesis. It comes from “Through the Looking Glass” by Lewis Carroll. In it, the Red Queen tells Alice, "It takes all the running you can do, to keep in the same place."

We've entered a different era characterized by responsible growth, a focus on profitability, stringent cost-control, and an emphasis on ROI. This shift heralds the resurgence of robust corporate governance. It's a positive change. The companies that adapt and strengthen under these conditions will not only succeed but will also contribute to enhancing the entire startup ecosystem.

The current economic climate is ushering in a wave of down-rounds, re-pricings, recapitalizations and closures. According to data from NYTimes, 3,200 private VC-backed U.S. companies have gone out of business in 2023. Startup shutdowns are up +50% year-over-year and up +300% over 2019. Many companies are currently relying on the capital they raised in the boom years of 2020, 2021, and early 2022. As we head into 2024, the companies that successfully secure funding will be those with robust metrics and well-established business models. For those companies that don’t meet the metrics I wrote about above, this funding is expected to run out in 2024. Why do I believe this is a positive thing?

The inflated valuations of 2021 have given way to a more sober market assessment. With the renewed focus on corporate governance and operational efficiency, companies are in a constant race to adapt to these evolving standards. Just like in the Red Queen hypothesis, if they fail to adapt and evolve, they risk failing. This continuous process of adaptation can lead to stronger companies overall, as they strive to outperform or at least keep pace with the changing demands and expectations of the market, thereby boosting the health and competitiveness of the entire startup ecosystem.

Investor-Friendly > Founder-Friendly

The days of founder friendly are shifting and the venture capital environment is tilting in favor of investors. This shift is evident in the prevalence of more investor-friendly deal terms and downside protections.

These are called dirty term sheets which are a twist on standard investment terms, heavily skewed in the investor's favor, and at some points can even be predatory. Investors wielding these terms will gain disproportionate control over the startup. A particular element is liquidation preferences. While it's normal for investors to recoup their investment first in a liquidation, combining this with liquidation multipliers and full ratchet anti dilution rights might become more common.

Of course, the investors are taking a risk investing (or saving) a startup so there is a fair argument to be made they should earn disproportionate voting rights, liquidation preferences, etc.

M&A

The possibility of an M&A supercycle seems increasingly likely. This trajectory is underscored by the data, which highlights a distinct shift favoring M&A over IPO exits.

This trend suggests a pivotal scenario for startups, particularly those facing challenges in securing additional growth funding. These companies may find themselves as prime targets in a landscape where private-to-private M&A becomes a critical strategy.

The current state of the IPO market amplifies this shift. Unless there's a revival in IPO activity, M&A emerges as a key avenue for liquidity for both investors and founders. We're likely to witness a surge in acquisitions, especially among companies aiming to enhance their AI capabilities. A notable example is Databricks' acquisition of MosaicML. This trend is expected to span various industries, with established companies seeking to bolster their AI capabilities.

Mark Carroll, VP Analyst at Gartner, highlights the global M&A activity, noting a decline from the peak levels of 2021 by 50%. He attributes this to macroeconomic and regulatory challenges. Yet, there's optimism for a resurgence, driven largely by a renewed focus on technology, particularly AI.

However, the regulatory landscape poses its own challenges. Despite most deals proceeding, there's an evident delay in approvals. The $69 billion acquisition of Activision by Microsoft exemplifies this, having faced longer than anticipated delays. Conversely, regulatory hurdles have impeded some major deals, like Adobe's attempted $20 billion purchase of Figma. Antitrust scrutiny remains a significant consideration in the M&A arena.

IPO

In 2023, IPO activity showed some bright spots with Instacart, ARM, Klayvio, and Birkenstock going public. However, their lukewarm market reception hasn't been a strong enough signal to encourage a broader wave of IPOs among private companies. 2023 mirrored historical low points in U.S. Tech IPOs, reminiscent of the dotcom and financial crisis periods, resulting in an all-time high backlog of private tech unicorns.

But now, according to Pitchbook, over 700 are lined up for IPO. EquityZen shows the global count of unicorn companies is set to exceed 1,200, with a combined valuation of $3.8 trillion. This indicates a growing need for liquidity solutions for early investors and expanding the investment pool for these burgeoning companies, contingent on favorable market dynamics.

Looking forward, a more stable market in 2024 could reignite interest in IPOs, providing opportunities for both retail and institutional investors to tap into emerging companies.

Potential IPO candidates include Fanatics, a leader in licensed sportswear and sports betting, Liquid Death, the unique canned water company with a "murder your thirst" branding and a $700 million valuation, as well as Reddit, ServiceTitan and Shein.

In short, if the IPO market were to open up and rebound, it would set off a series of positive ripple effects across the venture capital industry and the broader startup ecosystem. A rejuvenated IPO market would provide venture VCs and our LPs with significant liquidity. This liquidity is crucial as it validates the investment strategies and can be reinvested into new companies, fostering a cycle of innovation and growth. With more liquidity and higher valuations, venture capital firms may find it easier to raise new funds. If the IPOs are successful and have high multiples, it will send a signal of confidence in the market, which will lead to higher valuations for other companies considering going public. This will create employee wealth creation, in which these individuals may start their own companies or become new seed investors in the ecosystem.

Conclusion

Looking ahead to 2024, we're considering several macroeconomic scenarios and their potential impact on startups and VC investment:

1. A looming recession could lead to a broader market decline.

2. A softer economic landing might see a rise in IPOs akin to Klaviyo & Instacart, injecting slight growth as capital flows from funds.

3. We might encounter stagflation, a challenging mix of stagnant growth and inflation.

However, the economy will chart its own course, irrespective of predictions. My research leads me to a clear conclusion: as a private market investor, my focus should be on pinpointing exceptional companies at compelling valuations. The strategy is a flight to quality, backing specific sectors and founders with conviction. Opportunities always exist in businesses tackling significant challenges.

Historical data also favors private companies over the long term, mainly due to their early growth stages and higher potential upside. Supporting this view:

- Cambridge Associates reported that over 20 years, private equity outperformed the S&P 500 by 3.1% annually.

- McKinsey Global Institute found a 6.2% annual outperformance over a decade.

- Hamilton Lane Global Private Markets Review cited a 7.5% annual outperformance over 20 years.

We could also see a robust economic recovery, spurring consumer spending and business investments. Technological advancements, especially in AI, may open significant growth avenues for startups. Additionally, a rebound in IPOs and active M&A landscape could offer lucrative exit strategies, translating into substantial returns for investors.

We are looking for value in turbulent times and I am excited about it. I’m excited to venture forward.